So this graph shows the how the Total Economic Profit varies with the quantity produced.

Again – Common Sense tells you that to sell more coffee costs more (In the short run at least)

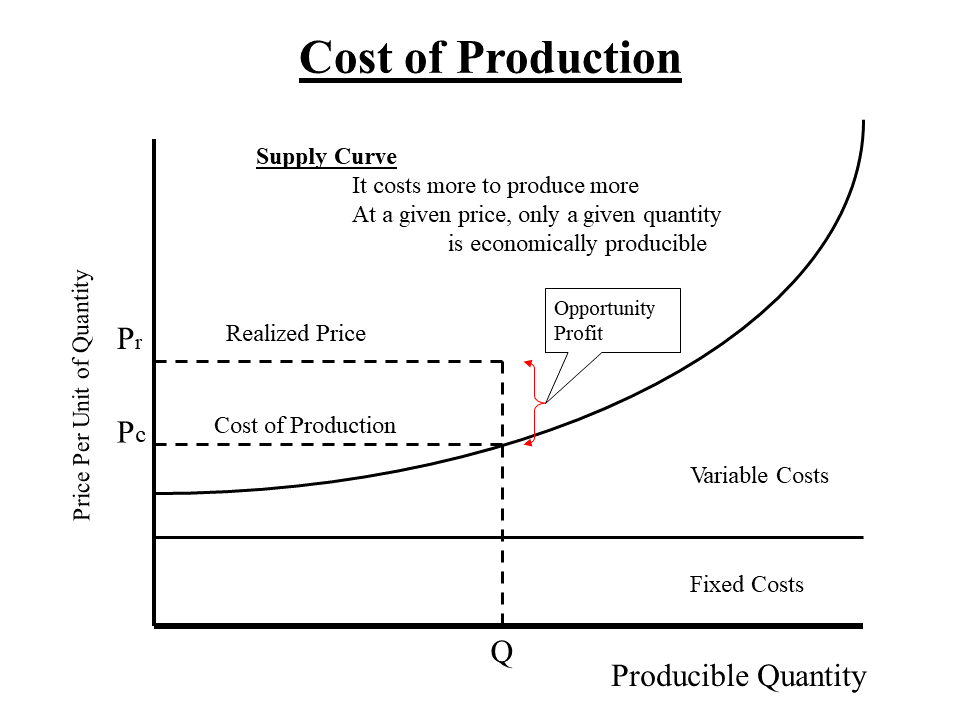

As With the Demand Curve I showed you, this Supply Curve is a generalized concept – averaged over all sorts of products, and all sorts of time frames.

The relationship between prices and Quantity is not a static entity – it changes over time as a result of changing costs of inputs, technologies, labour productivity,

and the changing circumstances of the business environment.

The shape of the curve is also flexible depending on the idiosyncrasies of the costs and technologies of producing various products and services.

Like with the Demand Curve, University Economics students spend an entire term studying the factors that influence the shape of that curve.

This depiction is an idealize aggregate of all of the unique supply curves of single suppliers offering for sale a single demandable commodity.

In the Short Term,

Fixed Costs are relatively constant, regardless of the quantity supplied.

Our Tim Horton’s franchisee has to pay her Fixed Costs regardless of how many cups of coffee she sells.

Variable Costs, of course, vary with quantity sold.

Each cup of coffee requires its own water, coffee, milk, paper cup, and staff labour.

The first cup of coffee has a minimum price – the franchisee has to cover the Fixed Costs and the Variable Costs of producing that single cup of coffee.

As more cups of coffee are sold, our Tim Horton’s franchisee has to cover additional costs.

Instead of picking up the coffee in a few tins on the way to work each morning, she has to pay for a big truck to deliver from the warehouse.

An existing business will be happy if they can sell at the Total Economic Cost of Production.

Someone planning to set up a new business will expect to be able to sell at a price giving them some Opportunity Profit

Otherwise, there is just too much risk, and not enough reward.

In the Long Run, of course, all costs are Variable.

And over time, the Supply curve will change as as a result of changing costs of inputs, technologies, labour productivity,

and the changing circumstances of the business environment.